Low-cost auto insurance in Tennessee is available from many top-rated companies. Instantly find the best prices for your vehicles and save hundreds of dollars. Regardless if you are currently without coverage, or have maintained the same policy with one carrier for many years, we shop all Volunteer State options so you pay less. Full coverage (collision and comprehensive) and state-minimum liability policies are offered at the cheapest available prices. Preferred, high-risk, and small-business options can also be viewed.

By comparing multiple companies, we can easily review the cheapest rates, and customize our quotes to match the vehicles you own. Typical savings for each driver can vary, based on the types of vehicles you own, driving record, available discounts, and several other factors. If you are presently uninsured, several companies offer same-day policies with minimum down-payments. If you are already covered, our free online quotes will provide all available discounts, resulting in up to 55% in savings. Commercial and group payroll-deduct options are also offered for selected employers..

The average cost of auto insurance coverage in Tennessee is approximately $150 per month. If collision and comprehensive are removed, the monthly cost reduces to approximately $115 per month. Multi-policy, good-driver, low-mileage, Senior, and multi-car discounts are the most popular ways to lower the premium. The Volunteer State is a "fault state," so you may be able to recover damages for personal injuries. Senior discounts help reduce rates for drivers that have reached age 55. When your home is covered by the same carrier, a discount of up to 20% may apply to both the auto and home policies. Rental and investment homes may also be eligible for additional savings.

Minimum Liability Requirements And Financial Responsibility Laws

If you own or operate a vehicle in Tennessee, the minimum allowed liability limits are $25,000 bodily injury per person, $50,000, bodily injury per accident, and $15,000 of property damage (TCA 55-12-102). When requested, documentation from a policy declarations page, binding agreement, or insurance ID card should be provided. Uninsured Motorist Bodily Injury (UMBI) of $25,000/$50,000 is also required. Although the number of uninsured drivers is decreasing, the coverage is still considered essential. Higher limits are typically required for leased vehicles. Proof of exemption from the financial responsibility requirement (DIFD-10) may be available.

Cash or bond may also be posted with the Department of Revenue ($65,000 required), in lieu of insurance, although this option is rarely selected. Failure to show proof of financial responsibility can result in a fine of $300, and your vehicle being towed. Also, your driver's license will be suspended when the DMV is notified. You also may not be able to renew the registration of the vehicle.

NOTE: These limits are commonly referred to as 25/50/15. When stopped by a police officer or registering your vehicle, you will be asked to provide proof of compliance. The TN Department of Insurance helps determine which limits are the most appropriate, and how often limits should be changed or increased. Regardless if you reside in the Smoky Mountains, the Graceland Mansion, or an apartment in Chattanooga, all drivers must comply. Lower limits are allowed in other states, although many states have recently increased their minimum required limits.

Driving without compliant coverage (including evidence of financial responsibility) can result in a license suspension and/or a $100 fine. Your registration can also be flagged (STOP) which may keep you from renewing. An SR-22 Filing or reinstatement of your license will then be required to regain driving privileges. Officially filed by your own carrier, after three years, the SR-22 will no longer be required if no additional license suspensions occur. Additional situations where an SR-22 is required include reinstating a license suspended for a DUI, excessive points, or failure to keep in-force complaint coverage. The electronic verification system makes it easier to determine who is diving uncovered.

If you do not own a vehicle, or it can not be driven and is currently being stored, you are not required to provide financial responsibility. An online questionnaire can be completed, to allow you to opt out of the liability insurance requirement. However, the Electronic Verification System will notify the Department of Revenue if you were required to place coverage on the vehicle. Lapses in coverage are not allowed. You van also call the Vehicle Services Center if you have lost your personal identification number (needed for online questionnaire). Your carrier has an NAIC code and it is listed on your policy, along with the date your coverage began.

If you just purchased a new vehicle, a temporary insurance card can be provided. If you are pulled over by a police officer, the ID will count as compliant coverage since the Electronic Insurance Verification System may not be updated yet. If the vehicle is self-insured, an online questionnaire can be completed to verify compliance. If you no longer own the vehicle, the Department of Revenue should be notified.

If the VIN from your registration does not match the vehicle VIN, the Vehicle Services Center should be contacted. If a letter is received from the Department of Revenue stating that your insurance coverage could not be confirmed, within 30 days an online questionnaire should be completed and submitted. Your carrier should also be contacted to verify the correct VIN is listed on the policy.

What Are The Most Expensive And Least Expensive Cities In The State To Insure An Automobile?

Rates are constantly changing, and determining, and predicting future rates is dependent upon many variables. However, we have listed below the Tennessee cities with the lowest and highest car insurance rates. We update prices quarterly.

Least Expensive Rates:

Afton

Athens

Bloomingdale

Blountville

Bluff City

Bristol

Butler

Cleveland

Colonial Heights

Cookeville

Crossville

Eidson

Elizabethton

Erwin

Franklin

Gallatin

Germantown

Goodlettsville

Gray

Greeneville

Johnson City

Lewisburg

Manchester

Maryville

Milligan College

Millington

Mooresburg

Mountain Home

Murfreesboro

Oak Grove

Paris

Pine Crest

Roan Mountain

Spurgeon

Smyrna

Trade

Wallnut Hill

Watauga

Memphis Car Insurance Rates Aren't Cheap -- But Affordable Options Are Available

Most Expensive Rates:

Antioch

Arlington

Atoka

Bartlett

Bolivar

Brighton

Clarksville

Cordova

Drummonds

Ellendale

Germantown

Goodlettsville

Jackson

Lakeland

Macon

Memphis

Middleton

Munford

Oak Ridge

Piperton

Rossville

Tipton

Washburn

Whiteville

Companies That Offer The Least Expensive TN Rates

Prices vary substantially for different ages, vehicles, and zip codes. Also, many carriers specialize in the non-standard (high-risk) market, while other selected carriers offer more competitive pricing in specific niches, such as Seniors, commercial vehicles, antique or custom cars, luxury vehicles, or auto-home combination policies.

Listed below (in alphabetical order), are companies that typically offer the most affordable auto insurance rates:

AIG

Allstate

Auto-Owners

Cincinnati

Erie

Esurance

Farmers

Geico

Liberty Mutual

Nationwide

Penn National

Progressive

Utica National

State Farm

Travelers

21st Century

USAA

Westfield

How Is Your Rate Determined?

Several factors are utilized when calculating your Tennessee car insurance quotes and other property and casualty products. Not all carriers use the same underwriting criteria, and sometimes, specific information you provide, will have a different impact, depending on the company. By customizing your quote, we can determine which policies provide the most cost-effective coverage. Listed below are common items that usually have the biggest effect on your rate:

MVR Report -- The number of tickets (moving violations) and at-fault accidents within the last three years can increase or lower your premium by hundreds of dollars every six months. Major violations may require you to keep high-risk coverage and possibly an SR-22 Bond. However, as the violations drop off your record, your policy can earn good-driving discounts, which will save money. Any high-risk driver that moves out of the household will also help reduce the rate. If excluded from the policy, they can not operate any of your vehicles.

Vehicle -- Newer cars and trucks typically are the most expensive vehicles to insure, although the value at the time of coverage is also a large factor. High-performance vehicles and commonly-stolen vehicles will also cost more. Smaller SUVs often have fairly low rates. Motorcycles, RVs, motor homes and off-road vehicles generally require a separate policy, although coverage may not be mandatory.

Age -- If you're under age 21 or over age 75, you will likely pay a higher rate. Prices tend to be lower for drivers between the ages of 35 and 60. The number of years licensed is also considered since regardless of age, the length of time licensed is always an underwriting factor. Drivers that just received their permanent license pay the highest premiums.

Liability Limits And Deductibles -- Although not recommended, choosing the minimum required liability limits will result in the lowest possible rates. Higher limits provide needed protection in the event of a lawsuit. The most common collision and comprehensive deductibles are $250 and $500, although higher options are offered. $1,000 deductibles will save money, and removing collision coverage should be considered on older vehicles with high mileage. Likewise, $2,500 deductibles should be considered on ultra-luxury vehicles, including the Audi A8, BMW 7-Series, Lexus LS, and Porsche Panamera.

Marital Status -- Married drivers (especially if under age 30) often are offered lower premiums than unmarried drivers. Divorced drivers do not pay a higher rate than single drivers. Single parents also do not pay a different rate than a single person. However, if one of the children drives, the rate will increase. Widowed drivers are not penalized.

Credit Score -- Many carriers utilize credit when underwriting policies. "Excellent" credit can lower the rate, since some research has shown that drivers with excellent credit are less likely to have an at-fault accident. Poor credit scores could possibly increase the rate, depending on the company. If your credit score substantially increases, the carrier should be notified. Credit scores above 800 may result in larger discounts.

County Of Residence And/Or Zip Code -- Like most states, Tennessee has specific areas where prices are low, and other areas where prices are often much higher. The rates you pay are are greatly influenced by where you live. More specifically, the more vehicle thefts and general claims in your area, the more expensive it will be to cover your car or truck. The hourly labor charge for repairing vehicles also will impact prices. Note: The counties with the largest populations (Shelby, Davidson, Knox, Hamilton, and Rutherford) generally offer competitive pricing, but not necessarily the lowest available rates.

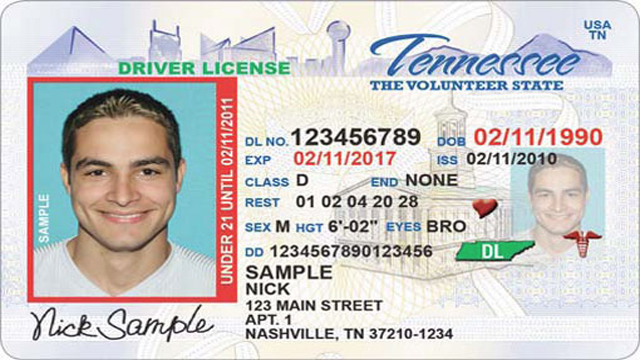

An Active TN Driver's License Is Required To Operate A Vehicle

Types Of Tennessee Driver Licenses

Standard Driver's License (Class D) -- The most common license which is a requirement to operate a vehicle. Weight of vehicle must be under 26,000 pounds (all passenger cars and trucks weigh less). Hazardous metals and more than 15 passengers must not be transported. SUVs, pick-up trucks, vans, and cars are generally included in the D Class. If you are under age 18, additional documentation may be required.

Teen/Graduated Driver's License (Class GDL) -- Commonly known as a "learner's permit," this license gradually allows young drivers to gain experience before receiving full privileges. Applicants must be at least 15 years old, and successfully pass visual and written exams. The GDL must also be kept for at least six months.

Teen/Graduated Driver's License (Class GDL) Intermediate Restricted License -- Multi-tiered program that gradually advances privileges of teen drivers as they obtain experience. Applicants must be at least 16 years-old and have had their learner permit for 180 days.

Teen/Graduated Driver's License (Class GDL) Intermediate Unrestricted License -Similar to the restricted license (above), although you must be at least 17 years-old, and have held the prior license for 12 months.

Hardship Driver License (Class H or XH) -- Approved in family hardship or specific needs situations. These licenses are issued to 14 year-old minors for driving Class De vehicles or Class M motorcycles.

Temporary Driver License (Class XD, XM, or Permit) -- For persons that are temporarily in the US with a special permit. Two forms of identification are required. The length of stay must also be indicated and proof of social security number must be presented.

Commercial Driver License (CDL) -- Larger vehicles typically require a CDL. The four types of commerce included are Intrastate Excepted, Intrastate Non-Excepted, Interstate Excepted, and Interstate Non-Excepted. DOT medical cards may also be required. An A/57 license may be required when trucks are hauling in excess of 10,001 pounds. Fingerprints and background checks may be required if hazardous materials are involved.

Motorcycle License (Class M) -- Applicants must be 16 years-old, and the license applies to motorcycles and other motor-driven cycles more than 50 cc. A road skills test is required to pass the license, and full-service Driver Service Centers are available (for testing) in many locations. An examination will include vision screening, motorcycle road/skills test, a pre-trip inspection, and a road rules knowledge test.

Applicants should read the "Motorcycle Operator Manual," which can be found at drivers license centers. Applications are also available at these centers. A written and road-skills test is required. A skills/road and knowledge test is waived if you have a valid driver's license. Four types of licenses are available. Persons with a valid driver's license can operate a motorized bicycle (50 cc or less) without an endorsement.

Full-Service Driver Service Centers are available throughout the state and offer knowledge testing and the needed applications. The road skills test can also be completed at these Centers. Several different examinations are offered, depending on the experience level of the applicant. A driver handbook and study guide are provided to help prepare for the examination. For current license holders, the examination will include a skills and road test, visual inspection, rules test, and vision screening.

Companies With The Largest Market Share

271 companies are licensed and approved to issue property and casualty policies in the state. Although the largest carriers do not always offer the cheapest prices, typically, their rates are very competitive in several, and often, most counties. Shown below, are, in order, the 20 insurers that hold the largest auto insurance liability market share in Tennessee.

19.50% -- State Farm

14.94% -- Tennessee Farmers Mutual

4.25% -- Progressive

3.91% -- Mountain Laurel

3.88% -- Geico Advantage

3.78% -- Allstate Property and Casualty

2.95% -- Erie

2.42% -- LM General

2.11% -- Safeco

1.99% -- USAA

1.96% -- Direct Insurance

1.82% -- Geico Choice

1.62% -- State Farm Fire and Casualty

1.56% -- Shelter Mutual

1.53% -- Trexis

1.53% -- USAA Casualty

1.35% -- Geico General

1.24% -- Auto Owners

1.12% -- Travelers

1.10% -- USAA General

Largest Homeowner's Market Share

25.2% -- State Farm

19.3% -- TN Farmers Mutual

3.1% -- USAA

2.9% -- Safeco

2.7% -- Liberty

2.5% -- Erie

2.3% -- Travelers

2.2% -- Farmers

2.0% -- Allstate

1.7% -- USAA Casualty

Drive Safely And Within The Speed Limit

Driver Slower And Safer

Crash data from the TN Department of Safety and Homeland Security (TDOSHS) provides fatality and alcohol-impaired driving information in all counties of the state. Types of crashes are divided into specific categories, including motorcycles, alcohol-impaired, Senior drivers, young drivers, and motorcycle crashes.

Shown below are the 25 counties with the highest number of total fatalities, injuries, and property damage. Naturally, higher-populated counties are more likely to be at or near the top of the rankings.

Shelby

Davidson

Knox

Hamilton

Rutherford

Williamson

Montgomery

Washington

Sumner

Madison

Sevier

Wilson

Putnam

Maury

Greene

Dickson

Hamblen

Cumberland

McMinn

Carter

Loudon

Jefferson

Bedford

Campbell

Cocke

Most Recent Rate Changes (2020)

Auto-Owners -- .70% increase

Direct Insurance -- 1.77% increase

Erie -- 3.80% increase

Farmers -- 4.0% increase

Geico Advantage -- .80% decrease

Geico Casualty -- .70% decrease

Geico Choice -- .50% decrease

Geico General -- 1.10% decrease

Liberty Mutual -- 12.25% increase

Progressive -- .05% decrease

Safeco -- 4.80% increase

Shelter Mutual -- .10% increase

State Farm Fire And Casualty -- .01% increase

State Farm Mutual -- 9.79% decrease

Travelers -- .70% decrease

USAA -- 5.05% increase

USAA Casualty -- 4.81% increase

Tennessee High-Risk Auto Insurance Plan (TNAIP)

TNAIP, available through licensed and registered brokers, provides policy coverage to applicants that have been unable to obtain and qualify for conventional car insurance in Tennessee. All companies in the state must share the risk, and underwrite applications that approximate their market share of in-force business. Applications can be submitted online, and once approved, your underwriting company is identified. High-risk and "non-standard" drivers typically find great difficulty when trying to find affordable, or any coverage! TNAIP provides an opportunity to secure a policy.

A valid driver's license and active registration are needed for consumers to apply for coverage. Also, proof of a denied application within the last 60 days, and proof that a policy premium has been paid within the last 12 months are required. The required application must be fully completed, with all questions answered. Affordable high-risk car insurance rates are possible, although prices may be initially high.

Applicants can not choose the carrier that issues their policy, since the selection is based on carrier market share. If full coverage (collision and comprehensive) is requested, an inspection must be completed. Also, if information is deliberately omitted from the application, for the next 12 months, another application may not be submitted.

When the policy is approved, coverage can continue for three years. However, if all drivers in the household have no moving violations or at-fault accidents, within 12-24 months, it's very possible you can obtain lower rates from a standard plan. Mandatory liability limits of $25,000 per person and $50,000 per accident, and $15,000 of property damage are required. Higher limits are also available. The minimum allowed collision and comprehensive deductibles are $100, although $250 or $500 is recommended. A cost-savings $1,000 deductible option is also offered.

There are three ways to pay the premium. The full annual premium can be made at the time the application is submitted. Of course, no further premiums would be due for 12 months. 25% of the annual premium may be paid with the balance divided into five equal installments. Also, 30% of the annual premium can be paid, with the remaining balance due within 30 days. A $4 fee is added to all installment payments.

Department Of Safety Offers Driver Improvement

Drivers that have 12 or more points on their record within one year, receive a written notice of proposed suspension. A personal hearing is offered, which may allow completion of a defensive-driving course to eliminate or reduce the period of suspension. Failure to appear at the hearing can result in a 6-12 month license suspension.

A juvenile driver (less than 18) with more than six accumulated points within one year, is transferred to the "Driver Improvement Program," and sent a proposes suspension letter. Attending an in-person hearing is required, and driving privileges can be suspended for up to six months. Completion of a defensive driving course will also be required. 10 or more accumulated points results in an automatic six-month license suspension.

TDOS-approved defensive driving schools are listed below:

A And O Driving School (Evensville)

A+ Defensive Driving School (Knoxville, Johnson City, Lenoir City, Kingston, Madisonville, Sevierville, and Maryville)

ABC Traffic School (Chattanooga, Nashville, Franklin, and Murfreesboro)

Access Granted Traffic School (Chattanooga)

Advanced Driving School (Memphis)

Defensive Driving Courses Inc. (Knoxville)

General Sessions Traffic Education Program (Nashville)

Knoxville Police Department (Knoxville)

Life Foundation Inc. (Kingsport and Johnson City)

Loudon County Sheriff's Office (Lenoir City)

TN Driver School Inc. (Rockwood)

Tennessee Point Values for non-commercial violations are shown below:

Speeding 1-5 mph above stated limit -- 1 point.

Speeding 6-15 mph above stated limit -- 3 points.

Speeding 16-25 mph above stated limit -- 4 points.

Speeding 26-35 mph above stated limit -- 5 points.

Speeding 36-45 mph above stated limit -- 6 points.

Speeding more than 45 mph above stated limit -- 8 points.

Driving slower than stated minimum -- 3 points.

Driving too fast for conditions -- 3 points.

Reckless driving -- 6 points.

Improper passing -- 4 points.

Failure to yield -- 4 points.

Improper turn -- 3 points.

Improper backing -- 3 points.

Inability to maintain control -- 3 points.

Passing a stopped school bus -- 8 points.

Leaving the scene of an accident -- 5 points.

Failure to stop at railroad crossing -- 8 points.

Failure to yield to emergency vehicles -- 6 points.

Failure to report a crash -- 4 points.

Speeding in a construction zone -- 2-8 points.

Child endangerment -- 8 points.

Fleeing law enforcement officer -- 8 points.

C.L.U.E.

C.L.U.E. (Comprehensive Loss Underwriting Exchange) is a report that provides seven years of claims information for vehicles and property. Insurers report when they have denied a claim, processed a claim, and payed money for a claim. When a consumer inquires about a deductible or policy information, it should not appear on the C.L.U.E. report. Typically, when a consumer applies for property and casualty insurance coverage, the carrier will order a report. Your claims history can potentially impact the cost of the policy and whether you will be accepted. The Fair Credit Reporting Act allows you to order a free copy of your personal report. Once received verification of information in the report should be verified for accuracy.

Your report will provide the following information: name, date of birth, carrier policy number, date that the accident or claim occurred, type of claim or loss, amount of money that was paid, address of property (if applicable), and description of items involved in the claim, including dwellings. Carriers disclose details regarding the amount of funds paid, and whether a claim was filed, and/or denied. The Fair Credit Reporting Act allows you to order (without charge) a copy of your most recent report.

Tennessee Move Over Law

The "Move Over Law" was passed 15 years ago and is contained in the "Failure To Yield To Emergency Vehicles" legislation. When an emergency vehicle is approaching, drivers must reduce their speed, and if possible, move to the nearest lane in a safe manner. The law is designed to protect police officers, firefighters, utility workers, and other emergency workers. The legislation was expanded 10 years ago to include service equipment.

The penalty of non-compliance is up to 30 days in jail and a fine as much as $500. The Counties that have issued the most violations are Knox, Shelby, Sullivan, Williamson, Robertson, and Smith. At the time the law was passed, 30 US states had passed similar legislation.